MoneySense is an award-winning magazine, helping Canadians navigate money matters since 1999. Our editorial team of trained journalists works closely with leading personal finance experts in Canada. To help you find the best financial products, we compare the offerings from over 12 major institutions, including banks, credit unions and card issuers. Learn more about our advertising and trusted partners.

In maintaining your planned allocations in a portfolio of ETFs, consistency matters more than precision. The post How often should you rebalance? appeared firstIn maintaining your planned allocations in a portfolio of ETFs, consistency matters more than precision. The post How often should you rebalance? appeared first

How often should you rebalance?

Building your own portfolio can feel like a rite of passage for a do-it-yourself investor. You skip the one-ticket asset allocation exchange-traded fund (ETF) and instead hand-pick a mix of low-cost, broadly diversified equity and bond index ETFs. You size them according to your time horizon and risk tolerance. On day one, everything lines up neatly.

But markets do not stand still. Over time, some asset classes outperform while others lag. Stocks may surge ahead during a bull market. Bonds may stabilize the portfolio during downturns. As those returns compound at different rates, the asset mix begins to drift from your original allocations.

An 80% equity portfolio can quietly become 85% or 90% equities after a strong rally. A rough year for stocks can tilt you further into fixed income than you intended. Performance swings, good or bad, can push your portfolio away from the risk profile you originally chose.

At some point, the mix no longer reflects your original plan. So, should you step in and rebalance?

Rankings

The best ETFs in Canada

read now

You might look to large ETF providers for guidance. The answers are not always clear. The Vanguard Growth ETF Portfolio (VGRO), for example, states that its 80% stock and 20% bond portfolio may be rebalanced at the discretion of the sub-advisor. That leaves plenty of room for interpretation.

Others are more prescriptive. The Hamilton Enhanced Mixed Asset ETF (MIX) uses 1.25x leverage on a 60% S&P 500, 20% Treasury, and 20% gold allocation. Hamilton specifies that it rebalances automatically if weights drift 2% from their targets. That is a tight band and implies frequent turnover.

But you are not running a fund with institutional constraints or leverage targets. You are managing your own portfolio. For most DIY investors, a simpler approach works better. Rather than reacting to every small market move, sticking to a consistent, time-based rebalancing schedule can reduce complexity and prevent decision fatigue.

In today’s column, we will look at why you should rebalance, how different time-based approaches have historically behaved, and why consistency often matters more than perfect timing.

Why rebalance your portfolio at all?

Rebalancing is the process of selling assets that have grown beyond their target weight and buying those that have fallen below it, such that you restore your portfolio to its intended allocation.

When you combine assets that are not perfectly correlated and periodically rebalance them back to target weights, you create what is referred to as a rebalancing premium. The underlying explanation has to do with how returns compound.

The arithmetic return is the simple average of yearly or periodic returns. It treats each period independently. The geometric return is the compounded growth rate of your money over time. It shows what you actually earn after gains and losses build on each other.

The arithmetic average of returns does not reflect the true investor experience. Investors live with the geometric return, which accounts for the effects of compounding and the impact of volatility.

Large swings in portfolio value widen the gap between arithmetic and geometric returns. By blending assets with different correlations and rebalancing them, overall volatility can be reduced. That narrows that gap and improves the compounding outcome. A simple back test illustrates this effect.

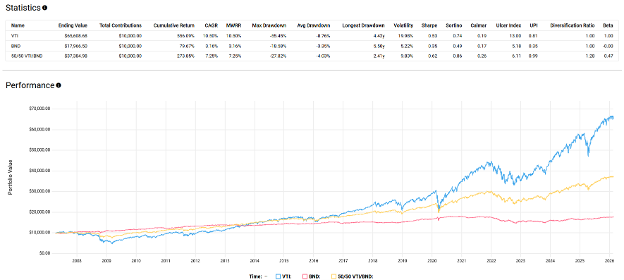

Source: testfolio.io

From April 2007 through February 2026, U.S. stocks returned 10.5% annualized. U.S. bonds returned 3.16% annualized. If you simply averaged those two numbers, you get 6.83%.

Now consider a portfolio that held 50% U.S. stocks and 50% U.S. bonds and rebalanced once per year. That portfolio returned 7.25% annualized over the same period. The difference between 7.25% and 6.83% of 0.42% per year reflects the benefit of combining and rebalancing the two asset classes rather than simply averaging their stand-alone returns.

The improvement also shows up in risk-adjusted terms. The all-stock portfolio delivered a Sharpe ratio of 0.53. Bonds delivered 0.35. The 50-50 portfolio, rebalanced annually, achieved a Sharpe ratio of 0.62. Even though its raw return was lower than 100% stocks, it generated more return per unit of risk taken.

When assets move differently from one another, periodic rebalancing can improve efficiency by moderating volatility and reinforcing disciplined buying and selling.

How often should I rebalance?

There are two approaches to rebalancing. Some ETF providers use band-based systems. As mentioned earlier, certain funds like MIX automatically rebalance when allocations drift by a fixed amount.

While that can work at an institutional level, for DIY investors it often invites more monitoring, more tinkering, and more temptation to second-guess the process. The more frequently you check whether you have crossed a threshold, the easier it becomes to let short-term market views creep into what should be a mechanical exercise.

A time-based schedule is easier to follow and less prone to behavioural bias. You choose a date and stick to it. But investors still fall prone to analysis paralysis—they fret over details like “how often?”

Featured TFSA Accounts

featured

EQ Bank TFSA Savings Account

Earn 1.50% tax-free on your cash savings.

Go to site

featured

TFSA GIC rate (1 year)

Earn a guaranteed 3.50% in your TFSA when you lock in for 1 year.

go to site

Best online brokers

Open your TFSA with one of the best online brokers in Canada. See our ranking.

Read now

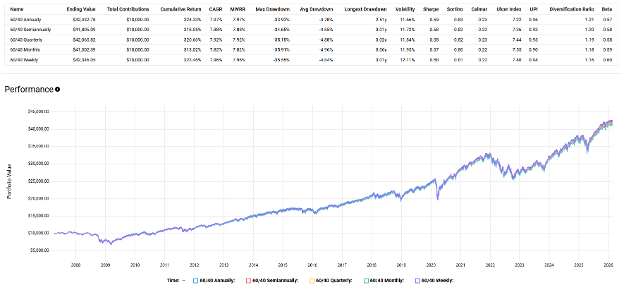

To test whether rebalancing frequency really matters, I back-tested five versions of the same portfolio from April 2007 through February 2026. Each held 60% broad U.S. equities and 40% U.S. aggregate bonds. The only difference was how often the portfolio was rebalanced: either annually, semi-annually, quarterly, monthly, or weekly.

The results were striking in how similar they were. Annualized returns across the five portfolios were within a few basis points of each other. Risk-adjusted performance, measured by the Sharpe ratio, ranged narrowly between 0.57 and 0.59. In short, the differences were minimal.

Source: testfolio.io

The rebalancing questions that never go away

The takeaway is straightforward: rebalancing across asset classes absolutely matters, but the exact frequency, within reasonable bounds, matters far less.

At first glance, this conclusion may seem at odds with a common critique of rebalancing: the idea that investors should let winners run because momentum is a powerful force in markets. The distinction lies in where momentum actually matters: within asset classes as opposed to across asset classes.

Equity markets, for example, can display persistent leadership effects, which is why market-cap-weighted indices often outperform equal-weighted versions during bull markets. Equal-weight strategies trim winners and add to laggards, which can work against momentum inside the same universe.

Across asset classes, the dynamics differ. Bonds, for instance, do not exhibit momentum in the same behavioural sense as equities. Their returns are largely driven by changes in interest rates and credit risk rather than trend persistence. Moreover, they are less correlated with stocks.

Rebalancing between assets with fundamentally different return drivers is therefore less about fighting momentum and more about managing risk and maintaining the intended portfolio structure.

Practical constraints on frequent rebalancing

That said, there are practical considerations, as our back test did not account for taxes or transaction costs. For example, in a non-registered account, selling appreciated positions to rebalance can create a tax liability. If your brokerage charges a commission for trading, that will also result in drag.

Still, even if trades are commission-free and assets are held in tax-sheltered accounts, higher trading frequency is not automatically beneficial. This is because every trade crosses the bid/ask spread.

This spread is the difference between what buyers are willing to pay and what sellers are willing to accept. It functions as an implicit cost of trading. While often small for highly liquid ETFs, it is never zero. More frequent rebalancing increases turnover, which means repeatedly paying this hidden cost.

Keeping turnover as low as reasonably possible remains sensible. The goal of rebalancing is risk control and allocation discipline, not constant activity. If annual adjustments achieve that objective, trading more often may simply introduce additional friction without materially improving outcomes.

Therefore, I am of the opinion there is little incentive for most investors to rebalance weekly or even monthly. An annual or quarterly schedule captures the bulk of the benefits while limiting turnover.

Personally, I prefer a quarterly schedule because it is easy to remember and automate. I set a recurring calendar reminder for the first trading day of January, April, July, and October. On that day, I log in, review the portfolio, execute the necessary trades, and move on.

Keep rebalancing and new contributions separate

Another question that often comes up involves new contributions and cash buildup. Should new money be used to top up whichever asset is underweight, or should contributions follow the original allocation with rebalancing handled separately?

From a behavioural standpoint, I think consistency is better. Directing contributions toward the underweight asset can feel rational, but it also introduces discretion. That discretion can easily drift into a mild form of market timing.

If the original plan called for an 80% equity and 20% bond mix, new contributions could simply follow that same split while rebalancing remains tied to the schedule. Otherwise, investors can find themselves between rebalance dates, noticing that an asset sits below its target weight and feeling the urge to “buy the dip.” That is where discipline can erode, turning a rules-based process into a series of ad hoc decisions driven by short term market moves.

Get rebalancing done quickly. Don’t fret over it and don’t second-guess yourself. There’s no need to back-test every possible interval or try to forecast every potential market outcome. Harvest the rebalancing premium, stick to a set schedule that reduces the temptation to tinker or time the market and, where applicable, keeps tax drag and transaction costs to a minimum.

Newsletter

Get free MoneySense financial tips, news & advice in your inbox.

subscribe now

Read more about investing strategies:

- Best robo-advisors in Canada for 2026

- Buffer ETFs vs. market-linked GICs: Which is better?

- If not bonds, then what?

- The ultimate couch potato portfolio guide

The post How often should you rebalance? appeared first on MoneySense.

Disclaimer: The articles reposted on this site are sourced from public platforms and are provided for informational purposes only. They do not necessarily reflect the views of MEXC. All rights remain with the original authors. If you believe any content infringes on third-party rights, please contact [email protected] for removal. MEXC makes no guarantees regarding the accuracy, completeness, or timeliness of the content and is not responsible for any actions taken based on the information provided. The content does not constitute financial, legal, or other professional advice, nor should it be considered a recommendation or endorsement by MEXC.

You May Also Like

Polymarket Acquires Dome to Boost API Infrastructure

The post Polymarket Acquires Dome to Boost API Infrastructure appeared on BitcoinEthereumNews.com. Polymarket acquired YC-backed Dome to expand its prediction market

Share

BitcoinEthereumNews2026/02/20 19:41

Silicon Valley Engineers Charged With Theft of Google, Tech Trade Secrets

The post Silicon Valley Engineers Charged With Theft of Google, Tech Trade Secrets appeared on BitcoinEthereumNews.com. In brief Federal prosecutors have charged

Share

BitcoinEthereumNews2026/02/20 18:48

Opendoor (OPEN) Stock Jumps 16% After Q4 Revenue Beat and Surging Acquisition Volume

TLDR Opendoor (OPEN) jumped 13–16.5% in after-hours trading after Q4 2025 earnings Revenue hit $736 million, beating Wall Street’s $595 million estimate by 23.7

Share

Coincentral2026/02/20 18:53